China Mobile Gaming | Jason Yen Interview

Interview with Jason Yen

This month I sat down with Jason Yen, a Channel Product Manager and Consultant for of MyGamez, a company helping non-Chinese games companies publish their games in China! We chatted about key publishers, marketing strategies, industry trends and more - check it out below!

🔑Key Topics Covered

Establishing the Market | Why do you think China mobile gaming is growing as fast as it is? What preferences do Chinese players uniquely have? (e.g. simple controls, PVP, IAP's over ad model)

Entering the Chinese Market | What expectations (if any) do non-Chinese companies have when looking to enter the Chinese market and common obstacles that they encounter.

Incumbents | The relationship that large publishers (Tencent + NetEase) have with regulators/government given that they act as gatekeepers to the market?

Publishing | Differences between the largest players in the android storefront market? How do developers know where/how to publish their games?

Closing Thoughts |What should more people understand about the Chinese mobile gaming market and advice for those looking to succeed in China?

Chinese Mobile Gaming Landscape

This post will be a review of the most important, and most cryptic games markets on the planet - the Chinese mobile gaming market. For as large as it is, it is not as simple as throwing an app on the Google Play Store and calling it a day. To be successful in the Chinese mobile gaming industry (of which, very few non-Chinese companies are), you need to understand the market with fluency and nuance that other markets simply wouldn’t demand of you.

From passing regulatory requirements to understanding the android app marketplace in China, there are many places that non-Chinese companies can go astray in their publishing strategy!

Let’s outline the market landscape by detailing the following before exploring what it means to succeed in this unique market in a subsequent post.

Market Sizing & Trends

Chinese vs Non-Chinese Companies

Key Developers & Publishers

Mobile App Publishing Platforms

Game Marketing Channels

📈Market Sizing & Trends

It’s no surprise that Chinese mobile gaming is growing at the rate it is. Any country pumping out 7-10% GDP growth for the past 5+ years should see increases in nearly all of their sectors. However with China specifically being so tech-forward economically and gaming forward culturally, the mobile gaming growth numbers we see are predictable but no less incredible.

So much of what contributes to the sheer market size of the Chinese mobile games industry is tied to something no other market (apart from India) can match - its population.

As we see on the right, a 663M total addressable market (TAM) of mobile gamers or 49% of China’s 1.4B population engaging with the medium is staggering.

The propensity to spend and average revenue per user (ARPU) of that 663M is another question entirely but as a starting point, having 2 US populations or 19 Canadian populations (my home country) worth of people engaging in mobile gaming is a testament to how colossal this global gaming center of gravity really is.

The graphic above shows the split between mobile vs console/PC games share of the Chinese gaming market in 2021.

Although consoles have been developing their presence in recent years with Sony’s PlayStation 4/5 and Nintendo’s Switch (less so Microsoft’s Xbox One/ Series X), China is still a mobile-first market, as we recognize in other Asian markets like South East Asia.

If you’re curious about the Singapore Games Industry - check out my post here!

But what is causing this growth and what could pose a risk to it? Let’s explore some market headwinds and tailwinds.

⬇️Headwinds

Regulators’ recent crackdown freezing of providing game publishing licenses. This resulted in the shut down of 14,000 gaming-affiliated companies in China, the South China Morning Post reports, consolidating that market further in larger companies and conglomerates even as it causes them to lay off workers and look overseas for business.

New regulation bans minors from playing games from Monday through to Thursday with China limiting online video games to three hours a week for young people. The revenue implications of this change are small according to Chinese gaming giants Tencent and NetEase, but could be detrimental to building long relationships with customers at a young age “We estimate about 5% of gaming revenue comes from minors under 18 years old, and we believe there is about 3% earnings impact to Tencent if we assume gaming contributes about 60% of total earnings,” investment bank Jefferies published.

⬆️Tailwinds

Economic development indicators such as GDP per capita cresting the $10k USD milestone suggest increased disposable income to be spent on high-end handsets, mobile games, and esports events/merchandise.

The widespread availability of 5G networks should be noted. The number of users for such networks has already surpassed 160 million (90% of the total number of users in the world). In 2021, the number of potential users for cloud games in China will reach 60 million.

Chinese Esports is blossoming as tech giants like Tencent and Alibaba are investing hundreds of millions of dollars into building eSports arenas and organizing tournaments and live streams. Thanks to these large-scale investments, eSports has become a part of the social life of Chinese young people with 26% of internet users watching streams of eSports events at least once per month.

🌎Chinese vs Non-Chinese Companies

As we’ve seen in Singapore, India, Korea, or even Africa, revenues flow back into the pockets of companies far from the markets they operate in. Koreans can enjoy League of Legends, an American-based title just as much as Indians can play Players Unknown: Battlegrounds from South Korea’s Krafton. A successful game is rarely just successful in the country it was developed in. When platforms like Google Play, Apple’s App Store, or Steam are so universal across markets, it can sometimes be as simple as localizing a game and throwing it up in another country’s app store to find success abroad.

The same does not apply to China at all. For many reasons we will go into later on, developers can’t simply flip a switch and enter the Chinese market. It’s too difficult for foreign companies to enter and succeed in China with this simple approach.

Revenue Split

“Western games are underperforming in mobile in China,” said Peter Warman, NewZoo’s chief executive, with experts pointing to foreign companies producing mobile games ill-suited to the country’s tastes and barriers to foreigners operating in China. But there is more to this story.

How do non-Chinese companies fare in this market and what prevents them from doing as well as home-grown games?

If we look at the top 15 mobile games by MAU below we recognize two things.

1) Less than half of these are made by non-Chinese developers. Many of them are partially owned (e.g. Activision) are entirely owned (e.g. Outfit 7) by a larger Chinese parent organization. Any game revenues stemming from these titles may flow to global pockets but at the end of the day the proceeds stay in China. These titles are:

Cross Fire Mobile | Korean

Sky: Children of the Light | American

Clash of Clans | Finnish

COD Mobile | American

Talking Tom Gold Run | Slovenian

2) All of these titles use Chinese publishers. We will explore this in detail later on, but names to note are Tencent and Net Ease, the largest 2 publishers. All of the publishers will have revenue share or royalty agreements imposed on revenues from these titles. Again, money staying in China.

A final point to highlight the importance of this nuance. ~50% of all the revenues of the Chinese mobile games industry come from the top 50 games.

As we see on the right, although there are a few non-Chinese companies who have entered China and found success, ~85% of game revenues from the top 50 games stay within Chinese borders.

This stems from a combination of 3 factors:

Chinese customers’ inherent preferences towards Chinese publishers. We will explore this below

The almost mandatory reliance on domestic publishing partners like Tencent NetEase which carry steep revenue split agreements which erode margins.

The political bias of the Chinese government to unsurprisingly promotes Chinese game developers over non-Chinese developers.

These factors reinforce themselves as well. The political bias means fewer non-Chinese games in the market, which means less customer familiarity with non-Chinese games which then requires non-Chinese developers to rely on publishing partners.

It’s a reminder for those looking to enter China to stay modest and humble. That even if you do crack the top 50 games, you can’t depend on the Chinese market to be the cash cow you hoped it would be, and if you do crack it like Supercell with Clash of Clan, you may have to forfeit equity as they did to Chinese Publisher Tencent.

Preferring Local over International

So why do non-Chinese companies struggle to succeed in the first place?

For one, Chinese mobile gamers prefer local publishers over Western ones. In a recent survey, when asked to express a preference, 86% of people said they preferred games from Tencent and NetEase to well-known Western publishers such as Supercell.

However, it is worth remembering that the Chinese government requires non-Chinese companies to work with either a local partner or to operate via a locally registered office, so many well-known Western games are released under a local publisher brand. For example, FIFA is published in China by Tencent, whereas gamers outside of China recognize the Electronic Arts and FIFA brands as inseparable.

There is also a clear preference for games that include Chinese designs and themes. Localizing games to the extent that character models and environments are changed to be more in tune with local tastes is always a good idea. Some of the most popular games in China feature storylines and characters taken from Chinese literature and history, and this is another way to cater to players in this market.

The Chinese government, which we’ll discuss later on, also just prefers to support local companies over international ones at the point of approval. In 2019, Chinese regulators approved 1,570 games, but only 185 were from overseas publishers.

👔Key Developers & Publishers

As we teased in the previous section, the Chinese mobile gaming market is top-heavy, which most of it’s revenue funneling through just a few games that are operated and published by a handful of publishers. The publisher side of the games market is very consolidated. So just who are these players?

Tencent

We’ve covered Tencent plenty of times on this blog so I’ll link out a few pieces that might be useful for those curious.

Tencent plays a key role as a Chinese market gatekeeper. The toll a company pays to pass said gate and enter the Chinese market? Equity. Many companies offer minority shares in their capitalization tables to enter the lucrative Chinese market. Many of these equity stakes remain simply as a minority but a few blossom into full-on acquisitions.

However, Tencent’s growth in recent years and equity-focused growth strategy has stirred up anti-trust concerns not only from China but to a wary America as well.

So much can be said about Tencent’s importance in the Chinese market but for now let’s keep moving, knowing they are the largest publisher with deep ties to the Chinese government and are behind much of the Chinese mobile and PC gaming markets.

NetEase Games

NetEase Games is a division of NetEase, a Chinese networking solutions company. They play less of a gatekeeper role like Tencent, opting to publish their own games, either through dedicated app storefronts or through direct download onto customer smartphones.

This is in part to avoid the steep revenue splits that they would have to fork over if they partnered with an Android storefront. This is also a way of creating brand value of NetEase Games’ titles by creating distance from the typical storefront distribution model which seems all too familiar to Chinese gamers.

Most of these agreements can be as low as 30% of all revenue all the way up to 60%. This means 30-60% of all transactions made through the game, like microtransactions, whilst being on a certain storefront will go to the storefront owner.

NetEase Games boasts an impressively diverse portfolio of mobile titles that all perform reasonably well as opposed to having a reliance on just one or two titles. Some of these include:

Creative Destruction

Identity V

Life After

Mihoyo

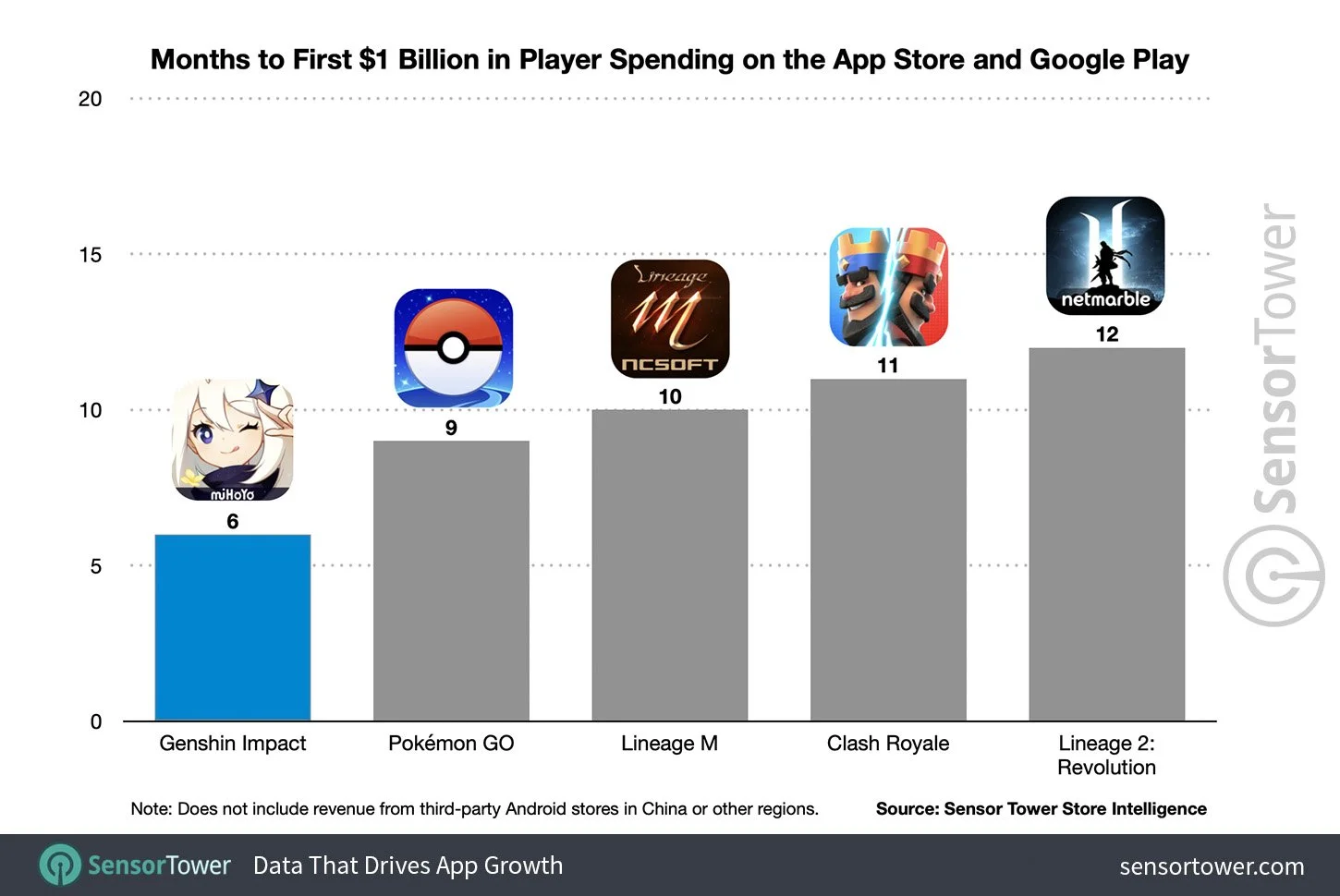

Mihoyo is the new kid on the block. They catapulted into global fame with their free-to-play RPG Genshin Impact when it launched in September 2020. It’s weeby as hell but that’s really the point. The anime art style, Breath of the Wild-esque exploration, and flashy combat have been incredibly well-received. The game currently boasts over 50M MAU’s and grossed more than $3.7Bn in its first year. It’s unique compared to other titles in the mobile market given that is available to play on PS4, PS5, PC, and even Nintendo Switch, following the lead of games like Fortnite or Roblox who dance in both console and mobile spaces.

Mihoyo is primarily known for its Genshin Impact title so it is difficult to say how well it could build out a diverse portfolio of titles in the long run. However, establishing such strong IP, loyal players, and business success in just 27 months from go-live is a great foot to start from.

Genshin Impact has been studied fiercely since its launch so if you’re curious to learn more about how it does well, check out Kalle Heikkinen and Erno Kiiski from Game Refinery’s analysis.

“Genshin Impact is getting things very right on mobile. That said, the fact that some of the game’s core competencies revolve around graphical fidelity and the core gameplay presents some risks.

Will players who join for narrative or exploration mechanics stay after the novelty of gameplay wears off or when credits start rolling? ”

🏪Mobile App Publishing Platforms

Although we’ll focus on Android publishing here, it’s worth calling out that Apple has a different version of the Apple App Store available in China for iPhone users. App and game publishers and developers must launch their apps on both versions of the Apple App Store to reach the entirety of the world market.

Unlike Apple however, the Google Play Store does not operate in China. Instead the market is comprised of hundreds of different storefronts all specializing in different categories.

What we see instead is a combination of pre-installed app stores from 2 sources:

Mobile phone OEM’s like Xiaomi, Oppo, and Huawei

Chinese tech giants like Baidu, Tencent, and Ali1baba.

Some other honorable mentions (not shown on the right)

Anzhi Market is a Chinese app store that has been around for many years. It has an active community that allows members to discuss and rate Android apps.

China Mobile is the state-owned telecom company in China that provides mobile services across Mainland China. China Mobile also has its own app store called MM Store. They also have one of the lowest revenue-share arrangements of all the most popular app stores, taking only a 30% cut.

All this variety can make it difficult for a game dev to know what platform is best for them. They all have different markets they cater to, with different requirements and different revenue-sharing terms.

That’s why a unique market has cropped up of companies consulting non-Chinese companies on how best to publish their games in China. An example is MyGamez, a Finnish company that offers game devs the following services to compete successfully in the Chinese market:

Android Publishing

Regulation & Licensing

Localization

China Specific Market Expertise

📣Game Marketing Channels

Marketing to the Chinese market could be another post altogether. It’s simply such a unique market filled with different customer expectations and preferred communication styles. That being said, we can look at some guiding principles that agencies have employed to bring non-Chinese games to China.

Partner With Key Influencers

In most of the world, we know it as Influencer Marketing. Paying a popular account on social media platforms like Instagram to promote your product or service. China calls this group of people Key Opinion Leaders (or KOL’s for short). Much like their global counterparts succeeding on YouTube or Tik Tok, KOLs have successfully dominated Chinese social media platforms like Weibo, WeChat, and live streaming apps in recent years.

The content published by the KOL can become viral on their specific spheres of influence. Unlike the west at least, there is a very dedicated network of agencies and media companies representing even small-time KOL’s. Where a brand might be able to simply DM an influencer with less than 10K followers outside of China, KOL’s in China are often represented by an agency that manages nearly everything about their brand.

In 2020, the New York Times put out a 12-minute video laying out the experience of these KOL’s. It isn’t gaming-related but gives you a morbid glimpse into this hyper-optimized machine that is Chinese KOLs.

Regarding gaming, developers and publishers often call on KOL’s for launch operations and get the first feedback about their game. Partnerships with gaming influencers can take the form of stress testing a game’s gameplay, announcing the next gaming trends, or even a step-by-step review of an entire game.

Chinese KOL’s often have very precise demographics that they resonate with, meaning the right KOL partnership on Weibo for example can yield very efficient paid traffic.

Given how data-rich most Chinese tech platforms are, delivering highly targeted ads across a network of KOL has been a very effective way of driving gaming traffic in recent years.

As an example, this is a high-level overview of a travel KOL’s follower profile. No doubt it is much more thorough on the backend but it should help illuminate why such a robust network of KOL agencies are required to reach every possible customer

Another key difference between KOLs and their Western ‘influencer’ counterparts lies in the payment structure for the KOLs. Whereas influencers typically receive a fixed amount of money for every social media post, KOLs directly partner with brands to receive appearance fees and generous commissions on brand sales (25–50%).

For the live stream shows on the KOLs social media channels, there is often an agreement in place ensuring the KOL selling during the live stream is offering the lowest price on the market, in the hope to boost sales figures. According to the KOL-management company Ruhan Holdings, these live stream hosts helped drive US$ 4 billion in sales in China in 2018.

Live Streaming & Esports

Live streaming was the very first topic I covered on this blog, in part because of how staggeringly important it is to understand Chinese Media. Two live streaming platforms, in particular, Douyu and Huya, are tailored to gaming (like Twitch.tv in other countries) and are common marketing avenues for games in China.

Mobile esports broadcasted through these platforms have also been gaining traction for quite some time and appeal to a wide range of demographics.

I recommend you check out this video from the Nanjin Marketing Group to get a grasp of the Douyu UI.

In Closing…

China as a country to the Western eye can be very mysterious. Its scale, growth, and ever international presence turn more and more heads every day. For some it’s for concerns regarding privacy (e.g. Huawei), for others it is their increasing foreign investment (e.g. Belt & Road Initiative). For me, it is the fact that one of the most important markets in the games industry is wildly underreported in the West. It is frustrating that the Western discourse around games centers around what is familiar, that being North America and European markets.

Although not many American companies have found success in China. that doesn’t mean it should be as discounted as much as it is right now. For people to have an informed opinion about games in 2022, it might be a good idea to know the 663M Chinese gamers are propping up the industry with $32Bn every year.

Big thanks once again to Jason Yen for his time and expertise. This post would not have been possible without this insight! 🥳